All Categories

Featured

Table of Contents

If you pick level term life insurance policy, you can allocate your premiums due to the fact that they'll stay the same throughout your term (Level term life insurance policy). And also, you'll recognize specifically how much of a fatality advantage your recipients will receive if you pass away, as this amount won't alter either. The rates for degree term life insurance policy will certainly depend upon numerous elements, like your age, health and wellness condition, and the insurer you select

As soon as you go with the application and clinical exam, the life insurance policy business will certainly assess your application. Upon authorization, you can pay your initial premium and authorize any type of appropriate documents to ensure you're covered.

Aflac's term life insurance policy is convenient. You can pick a 10, 20, or 30 year term and enjoy the added satisfaction you deserve. Working with a representative can help you find a policy that functions finest for your needs. Discover much more and obtain a quote today!.

This is despite whether the guaranteed person passes away on the day the policy starts or the day prior to the plan finishes. Simply put, the quantity of cover is 'level'. Legal & General Life Insurance Coverage is an example of a degree term life insurance policy policy. A level term life insurance policy plan can fit a variety of situations and requirements.

Why do I need Level Term Life Insurance Protection?

Your life insurance policy policy might also create component of your estate, so can be subject to Estate tax found out more about life insurance policy and tax. Allow's check out some features of Life Insurance policy from Legal & General: Minimum age 18 Maximum age 77 (Life insurance policy), or 67 (with Critical Health Problem Cover).

What life insurance policy could you think about if not level term? Lowering Life Insurance can assist secure a settlement home loan. The quantity you pay stays the very same, yet the degree of cover lowers approximately according to the method a payment home mortgage lowers. Decreasing life insurance policy can help your liked ones remain in the family home and stay clear of any kind of additional disruption if you were to die.

Term life insurance policy gives coverage for a specific time period, or "term" of years. If the guaranteed individual dies within the "term" of the policy and the policy is still effective (active), after that the survivor benefit is paid out to the beneficiary. This type of insurance policy usually permits customers to originally purchase even more insurance coverage for much less money (premium) than other sort of life insurance.

What is the process for getting Level Death Benefit Term Life Insurance?

If any individual is relying on your earnings or if you have obligations (financial obligation, home mortgage, etc) that would be up to someone else to handle if you were to pass away, after that the response is, "Yes." Life insurance policy acts as a substitute for earnings. Have you ever before calculated just how much you'll gain in your life time? Commonly, over the course of your working years, the solution is normally "a fortune." The potential danger of losing that gaining power profits you'll require to fund your family's biggest objectives like acquiring a home, paying for your youngsters' education and learning, minimizing financial debt, saving for retired life, and so on.

Among the main allures of term life insurance policy is that you can get even more insurance coverage for much less money. The protection expires at the end of the plan's term. One more way term plans vary from entire life or irreversible insurance policy is that they usually do not build cash money value gradually.

The concept behind lowering the payout later on in life is that the insured prepares for having lowered insurance coverage requirements. As an example, you (with any luck) will certainly owe much less on your home mortgage and various other debts at age 50 than you would certainly at age 30. Therefore, you could pick to pay a lower costs and reduced the quantity your recipient would get, due to the fact that they wouldn't have as much financial debt to pay on your part.

What should I know before getting Level Term Life Insurance Coverage?

Our plans are made to fill up in the voids left by SGLI and VGLI strategies. AAFMAA works to understand and support your unique economic goals at every stage of life, customizing our solution to your special situation. online or over the phone with one of our military life insurance specialists at and discover more regarding your army and today.

Level-premium insurance coverage is a type of irreversible or term life insurance where the costs remains the exact same over the plan's life. With this kind of coverage, costs are thus guaranteed to stay the same throughout the contract. For an irreversible insurance plan like entire life, the amount of protection supplied boosts gradually.

Term plans are also commonly level-premium, but the excess amount will continue to be the same and not grow. The most typical terms are 10, 15, 20, and thirty years, based upon the needs of the policyholder. Level-premium insurance coverage is a kind of life insurance in which premiums remain the very same rate throughout the term, while the quantity of insurance coverage offered boosts.

For a term policy, this suggests for the size of the term (e.g. 20 or three decades); and for a long-term plan, up until the insured passes away. Level-premium plans will normally cost even more up-front than annually-renewing life insurance policy plans with regards to only one year at a time. However over the long run, level-premium settlements are usually a lot more cost-effective.

Can I get Level Term Life Insurance For Seniors online?

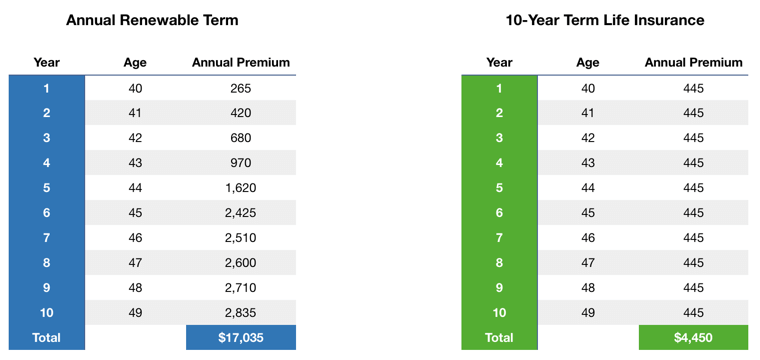

They each seek a 30-year term with $1 million in insurance coverage. Jen purchases an ensured level-premium policy at around $42 monthly, with a 30-year horizon, for a total amount of $500 annually. Beth figures she may just need a strategy for three-to-five years or up until full payment of her present financial obligations.

So in year 1, she pays $240 each year, 1 and around $500 by year five. In years 2 through five, Jen remains to pay $500 per month, and Beth has actually paid an average of simply $357 annually for the same $1 million of coverage. If Beth no much longer requires life insurance policy at year 5, she will have conserved a great deal of money about what Jen paid.

Annually as Beth obtains older, she deals with ever-higher yearly premiums. At the same time, Jen will certainly remain to pay $500 each year. Life insurers have the ability to provide level-premium plans by essentially "over-charging" for the earlier years of the plan, collecting more than what is needed actuarially to cover the danger of the insured passing away during that early duration.

2 Expense of insurance coverage prices are established using methods that vary by company. It's essential to look at all factors when reviewing the total competitiveness of prices and the worth of life insurance protection.

How do I choose the right Level Term Life Insurance Calculator?

Like many team insurance plans, insurance policy policies supplied by MetLife contain certain exclusions, exemptions, waiting periods, decreases, limitations and terms for maintaining them in force. Please call your benefits administrator or MetLife for expenses and full details.

{kind=link}

Latest Posts

Term Life Insurance Instant

Whole Life Insurance Quotes Online Instant

Instant Term Life Insurance Quotes Online